-

17 Ways to Get Out of Debt Fast and Save Money

Debt is money owned to the lender with outlined obligations such as time and interest charges.

Debt is money owned to the lender with outlined obligations such as time and interest charges.There are many ways to get out debt, but the most difficult thing is being consistent when you cannot see any immediate results. Staying on budget and tracking every dollar, can be the start of empowering your journey towards success.

Debt can be an overwhelming burden that affects every aspect of our financial lives, from our ability to save for the future to our overall peace of mind. For those facing the weight of debt, finding a way out and saving money in the process is a top priority.

These strategies encompass a wide range of techniques, from creating a solid budget and prioritizing high-interest debts to exploring debt consolidation options and maximizing your income. Whether you’re grappling with credit card debt, student loans, or any other financial obligations, these insights are designed to empower you to regain control of your finances, break free from the shackles of debt, and set yourself on a path towards a more prosperous financial future. So, let’s embark on this journey to discover the ways to get out of debt fast and save money along the way. Below are some effective tips that can easily help you speed along into crushing debt. There is no greater feeling than being debt-free, and yes it takes tremendous planning.

.

1. Educate Yourself

Understand Your Debt

The first step would be to know exactly how much in debt you are. List all your debts by the due date, interest rate, amount and minimum payment. This will give you a clear indication of how much debt you have to pay and the associated interest.

Educate Yourself about Debt

You need all the help you can get in order to demolish your debt and a little help goes a long way. There are many laws and regulations that protect you when facing either debt crisis or finding new ways to pay off debt. The best way to research is to first identify which category your debt is in and then find corresponding laws or regulations that protect you. This is extremely helpful if you decide to negotiate with your lenders. Below are some examples

- Student loan forgiveness

- Fair debt collection practices act

- Debt Consolidation (understanding the pros and cons)

Pull Up Your Credit Report

This should be done on a yearly basis, but in this instance, the purpose is to know exactly what you owe and if there is anything that is being reported that you were not aware of. Dispute any errors as they have a negative impact. The main objective is to increase your score, honestly helps with the interest rates, you will be surprised how much money you can pay towards interest.

Take a Financial Class

There are many ways to get financially educated and honestly, there is always something to learn. The best approach is to find various forms of obtaining financial knowledge that you are comfortable with, whether be it a podcast, a book or a financial blog. Learn new ways in the current phase you are in, for instance, if you are in debt, then debt repayment knowledge would be helpful.

.

2. Money Management

Stop Using Your Cards

Start using the cash method to cover all your expenses. Using your credit card continuously is just getting deeper into a rabbit hole. This strategy is best served with creating a budget and knowing exactly what your expenses and budget for them accordingly.

Select a Debt Repayment Method

There are many methods of paying down debt, such as debt avalanche or debt snowball. The debt avalanche is an accelerated debt repayment process. You pay off in order of the highest interest to the lowest. Whereas, with debt snowball, you pay off your debt from the smallest balance to the largest one, regardless of the interest rate. In all honesty, there are numerous methods of paying down debt, as long as you pay down the debt, the method becomes an option of choice that best suits you.

Credit Card Balance Transfer

This is when you acquire a zero percent credit card and use that card to pay off a loan with interest. This is a great way to save money when it comes down to interest, but you have to be very careful on how to implement the strategy in a way that is beneficial. The best approach is to have enough funds to pay the whole credit card amount in full before interest is applied.

Refinance Your Debts for a Lower Interest Rate

If you cannot qualify for the zero balance transfer, this is the next best option. Negotiate for a better interest rate and terms. Be careful when it comes to refinancing, some experts advise not to take a HELOC loan and pay down credit cards with it, because if it leads to bankruptcy, you might lose your house to credit cards. Below are some points to negotiate over

- Duration

- Interest rate

- Monthly payments amounts

Stop Contributions

This may be a hard concept to accept but if you do the math, it tends to showcase that debt is more expensive than the returns in a stock market. The average returns in a stock market are roughly 7% per year, whereas, credit card debt charges are roughly 14% to 25%. The best approach would be to stop all contributions to investment accounts and savings accounts (after funding your emergency fund) and then divert all your money into debt repayment.

.

3. Lifestyle Changes

Cook at Home

Eating out is a sure luxury when you are in debt, you cannot afford it. If you tally all the amounts spend on eating out, more than likely it is enough to cover your grocery bill. The best way to save money when it comes to grocery shopping is to set a budget and meal plan. This is usually an expensive bill if not well managed. It is always best to grocery shop with a list and meal prep for meals during the week.

Cancel Subscriptions

Time to be creative and cancel any subscriptions such as cable, magazines, streaming services and divert that money toward your debt. It might be time to pick a hobby that is free or spend more time outdoors or a second job. Most people think that since the amounts are so small it will not make a dent in repayment, but the most favored philosophy is that a little goes far. Make your money work for you.

No Vacations or Upgrades

Going on vacation it’s pretty inciting, but that only translates to one being in debt longer. Better yet to use that money and pay down your debt and opt for something that is more reasonable such as a staycation.

Downsizing

Cutting down on your expenses and increasing debt repayment amounts is a fast track method of cutting down debt. Evaluate your current status and downsizing may be a necessity. Examples of downsizing include:

- eliminating a car,

- Renting out a bedroom to get extra cash – such as Airbnb

Cut Down Luxury Items

This is difficult for most people, even though you are in the mindset of aggressively paying off debt, many people want to still enjoy certain aspects of life. Below are some luxury aspects you can do at home

- Do your own nails

- Do your own hair

- Bring your own lunch

- Make your own coffee at home

- Eliminate activities that are not part of the needs

Social Life

This can be a budget drainer, honestly, there is no fun in being so disciplined and not enjoying a quality life, but debt is a bigger problem and very costly. To enjoy the social aspect of life, it is best to carefully plan and budget carefully. There are many sites that offer discounts and many cities have lists for free activities. Whether its a date, brunch or a concert there are discount websites that offer extremely reduced prices. The best approach is to plan out your activities ahead of time and secure the best deal you can get.

.

Related articles:

- Effective Personal Budgets

- 10 Effective Personal Budget Tips

- 10 Investments that Create Wealth

- How to Save for Money for Big Events in Life

- How I Got a Six-Figure Raise 80k to over 150k

4. Make Extra Money

Increase Income

To expedite the process it is vital to increase your income and any small amount helps. There are certainly numerous ways to make additional money but the best place to start is what you are good at and or what can easily bring cash as fast as possible

Sale Items

It is much easier to sell unwanted items for the best prices than before. The best process to select the most profitable platform is to verify what cost is associated with selling your items. Garage sales are not the only way to sell items and sometimes you are leaving money on the table.

- Letgo

- OfferUp

- CPlus

- 5miles

- eBay

Tutoring

Take an inventory of your skills and certain them into making money. Research your desired area of tutoring, create an online portfolio, set your prices, choose methods of how you will tutor online or in-person and market yourself.

On-Demand Tasks

Join apps where you can specialize in completing certain tasks, you can easily customize your work schedules and you can do this when you have free time for instance,

- Task Rabbit

- Personal Shopping

- House Sitting

- Pet Walking

Driving

You can either be a weekend or after work driver and set your own hours. Work in areas that have a higher per hour rate like a more metropolitan place or during rush hours where the rates go up. Some companies include

- Lyft

- Via

- Uber

.

5. Motivation

Accountability and Support

Paying debt off is a hard task to do, especially when you are constantly living within parameters that do not allow you to fully enjoy life or living past the bare minimum – that is no easy task. Find like-minded people that will encourage and support you during your debt repayment process, as you can share resources, advice, and motivation.

Milestones

In setting a goal, there should be smaller actionable tasks that should be completed first. Take the time to set up those tasks and set out your milestones as well. For instance

Goal identify your main budget goal e.g payoff credit cards Task breakdown your goal into more manageable tasks e.g first paying the high balance credit card Milestone your milestone can be after paying every $10,000 (then you can reward yourself) Reward Your Self

After paying off one card or reaching a certain number, reward yourself. You have certainly earned it and rewarding yourself can truly be a motivator. Set rewards that are truly fulfilling, such as a spa date, great dinner or a night at broadway – something that really means a lot to you, just to celebrate your achievements. You are doing great and keep going.

.

6. Top Question on How to Get Out of Debt

There are many issues, challenges when it comes to getting out of debt. The below questions are some of the top questions and or concerns, but one of the surest way is to create a research, set a goal then create a plan.

Get Out of Debt Living Paycheck to Paycheck?

The best way to get out of debt while living paycheck to paycheck is to start a strict budget that includes all your expenses to the penny. The reason being that we tend to waste money on little small buys which actually tend to add up. Below are some types of budgets to consider:

-

-

- Zero based budget

- Cash envelope budget

- Snowball debt payment method

- paying your debt every two weeks (however small the payment is – it helps in the long run)

- Calling your creditors if the t have a debt relief program (some companies may offer you to skip payments)

-

Who can help me Get out of Debt?

The first place to seek help is your creditor, verify if they have any financial programs that can help. The next best approach is to seek outside help, such a state or federal agencies that may help you in any financial assistance. The last step would be to contact debt management companies and verify the best solution to manage your debt the correct way.

KEY NOTE – before you contact debt management companies be cautious what their requirements are and if there are any related fees.

What Debt Should I Payoff First to Raise My Credit Score?

If you have different creditors, it is best to payoff the debt that has the lowest amount, mainly because you are able to pay it faster. Once a debt is paid off, it is reported as such on your credit bureau and this raises your credit score drastically.

Does Paying All Debt Increase Your Credit Score?

Paying all your debt does increase your credit score as the debt utilization score used to determine your credit rating decreases. The lower the score the better. This is the most crucial aspect to be note, your credit score may decrease instead of increasing if you payoff debt and close the account. this is usually applicable to credit cards

The best approach would be to payoff all the balance on the account BUT DO NOT CLOSE THE ACCOUNT. If you hardly use the credit card, the company might close it for you, it’s advisable monitor your card usage.

Why did My Credit Score Drop After Paying Debt?

Part of your credit score is calculated by having revolving debt. Once you payoff your debt and the the account closes, this may impact your credit score calculation. The best way is to maintain credit cards that you frequently use but just make sure you pay it off each month.

Summary

There are many ways to save money and get out of debt, but the first step towards financial freedom or growing wealth is to have a plan that can be broken down into manageable tasks. When it comes to debt repaying, the first step has to understand what you truly owe, learn about the extent and cost of your debt, create a great financial plan and finally getting a supporting system.

.

Cheering To Your Success

Brenda | www.DesignYourFinances.com

Let’s Connect on Social Media! | Pinterest |

–

QUOTE OF THE DAY

-

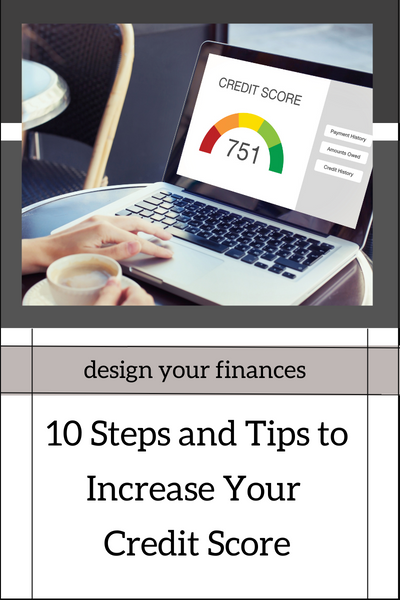

10 Steps and Tips to Increase Your Credit Score

A credit score is a three digit number that correlates to how financially trustworthy a person or company is.

A credit score is a three digit number that correlates to how financially trustworthy a person or company is.The higher the credit score the cheaper your interest rates are and more financially trustworthy.

Your credit score is a powerful financial tool that can open doors to better interest rates, higher credit limits, and financial opportunities. A good credit score is not only a symbol of financial responsibility but also a practical asset that can save you money in the long run. In this comprehensive guide, we will explore ten essential steps and tips to help you increase your credit score.

From understanding the factors that influence your score and diligently monitoring your credit report to managing your credit utilization and strategically using different types of credit, these insights are designed to empower you to take control of your creditworthiness and work toward a higher and healthier credit score. Whether you’re looking to improve your score for future financial goals or need to repair past credit mistakes, these strategies will provide you with the knowledge and tools to enhance your credit profile and enjoy the benefits of better credit. So, let’s embark on this journey to discover the steps and tips that can help you increase your credit score and unlock financial opportunities.

.

1. The Basics

There are 3 main credit bureaus TransUnion, Equifax and Experian and they generate a credit report for you by evaluating your credit score. The credit score is calculated from different criteria which include:

- credit usage

- types of credit

- length of credit

- recent inquiries

- payment history

The above-listed criteria are further analyzed to determine if you are creditworthy, obviously, if you have a higher score, you are regarded as a more trustworthy borrower. The scores are segmented into different groups such as:

Rating Score Poor 300 – 579 Fair 580 – 669 Good 670 – 739 Very Good 740 – 799 Exceptional 800 – 850 Of course, the higher your score is the lower the interest, cheaper the loan and vice versa, the lower the score, the higher the interest and the more expensive the loan is.

.

2. Credit Usage

This covers how much of the available credit you can use. It is widely advised not to use your credit to the max and worst not pay off the full balance, as this translates to poor credit management and reflects as you being poor in cash. Carryover balance is great for the lender as they charge so much interest, but to the credit bureau, it reports the inability to pay off. Having great credit usage is in having a credit credit score and it opens more avenues for you when you want to get different types of credit.

.

3. Revolving Utilization

This is an indicator of how much you owe on your accounts. The amount you owe lenders is one of the most important factors that impact your credit and makes up about 30% of your FICO Score. The revolving utilization score is determined by:

- The total credit limit

- The total balance owed on your revolving accounts

For instance, if you have a total credit limit of $30,000 and you have used up $22,136 that means you have a revolving utilization rate of 69% of your total credit limit.

TIP – Using most of your available credit is a sign of very high risk and that is considered poor. The total balance on your last statement is generally the amount that will show in your credit report, even if you pay in full each month.

.

Related articles:

- Effective Personal Budgets

- 10 Effective Personal Budget Tips

- 10 Investments that Create Wealth

- How to Organize Your Blogging Business

- How to Save for Money for Big Events in Life

- How I Got a Six-Figure Raise 80k to over 150k

4. How to Build Credit Score

When you apply for a job you provide a resume with listed experiences, this gives an overview of what you can do. The same principle with this section of the credit report, it essentially reports your past credit behavior. Creditors want to know you can be responsible and managing a mix of different loans, showcases your ability. This makes up to 10% of your total score. The FICO calculation accesses the type of credit as either installment loans or revolving accounts.

Installment Loan

With this type of loan, you borrow the money once and pay it off over a period of time. This type of loan includes auto loans, student loans, or mortgages.

Revolving Accounts

This type includes accounts such as a credit card, or department store cards. The main purpose or definition is that the loan is always available, you keep borrowing as long as you can repay your creditor according to the terms.

Be mindful of other factors regardless of the type of loan it is, it all boils down to you owing the lender money and rules can easily change. They make money off you and the longer you are in debt the better for your creditors, as your debt generates revenues.

TIP – Generally, opening new credit accounts that you do not need, will not necessarily improve your score. Do the research before opening.

.

5. Length of Credit

Just like when applying for a job, the more years of experience you have the more leverage you have when it comes to the position and salary negotiation. The same principle is applicable here. The longer the credit history you have, the better. The length of your credit history makes a great impact when it comes to calculating your score, which is 15%

In addition to the length of your credit, below are some points taken into consideration:

- The age of your oldest credit account

- The age of your newest credit account

- The average age of all of your credit account

TIP – Even though you pay off your credit cards, it is best to keep the oldest card open. I would suggest a credit card that does not have an annual fee.

.

6. Inquiries

This makes about 10% of your score.

This is one of the most known factors that can harm your score. There are two forms of it, either hard or soft inquiry. There are two types of inquiries, a hard inquiry is when a creditor pulls up your credit, (of course this is to verify if you are credit-worthy) and a soft inquiry is when you pull your own credit report, usually, there is no fee associated if you pull it once a year. There are many websites that offer that service, be sure you are pulling from a credit worth source such as Credit Karma, or Annual Report.

TIP – You generally do not want to have many inquiries made on your account. Hard inquiries made by a lender, can only be done with your permission. Therefore, be careful of what you give your consent to and state when your authorization to pull your credit report expires.

.

7. Paying History

This makes at least 35% of your score.

Well, this one drives the score and if you miss a payment, it will severely bring it down.

Consistently paying creditors on time is the most important factor in determining your credit score The calculation is based on the number of accounts with missed payments over the length of your credit and below are the determining factors:

- Amounts owed on delinquent accounts

- Collections and negative public record information, such as tax liens, repossessions, charged-off accounts

TIP – This is a well-known factor that, paying your bills on time demonstrates a good payment history. The total balance on your last statement is generally the amount that will show in your credit report, even if you pay in full each month.

Due to the increasing cases of fraud, most of us live in a state of constant concern what if my financial details are leaked or the recourse of such invasion. I was personally affected when there was an Experian Data Breach, the worst part of the whole process was the mundane responses I kept getting and not a full answer whether I was protected. Luckily, no financial damage was done, but that led me to investigate other options for protecting myself. The list below is not exhaustive but surely a start.

.

8. Ways to Protect Your Credit Score

Pulling Up Your Credit Report

The first option would be to pull your credit report, this will give you an overview of exactly what you owe and or other mistakes that are being reported. If you identify an error, you do have the right to dispute and the credit bureaus have 30 days to resolve the dispute, if no response in 30 days, then by law they should remove it. As I stated earlier, you do have the right to pull up your credit and Free Annual Credit and Credit Karma you can pull it once a year free of charge.

Having Several Alerts from Your Accounts

There are many ways banks or financial institutions are offering services that protect their customers. This has personally become handy as I have experienced unauthorized usages. I was able to have the charges removed. I have alerts of transactions that are over a dollar, therefore, I monitor all transactions coming through. In addition, my bank contacts me if there is a suspicious charge and I have me confirm if its a true transaction, if not it gets declined. Contact your financial institution and activate alerts that offer more protection on your account.

Black Market Social Security Number Scanning

There other services that are currently being offered, such as having your social security being scanned to see if it is on the black market. Information stolen is grouped into various categories and prices. Some banks and credit bureau’s have services that offer to scan your social security number. Conduct detailed research and understand the requirements, the best approach, would be to do it with a trusted financial institution, such as your and not just another website.

Separate Bank Accounts

Due to my personal exposure as a victim of financial fraud, I have since changed my banking habits. I have different bank accounts with different banks. That includes a household account that solely deals with paying bills and all other transactions. I transfer funds each month (or when needed) from my Bank A to Bank B. If my household account is affected, at least I will not suffer loses beyond the balance in that account as it does not have more than what I need in a month.

The same principle when it comes to credit cards I use only one when doing online shopping. To take further measures, I have a PayPal account where that one credit card is attached to, therefore all my online shopping is processed through PayPal. The reason I favor this method, its because my credit information is not scattered everywhere and it is easier to monitor. The card attached to PayPal has a lower credit limit than my other one.

Freezing Your Account

This is probably the best one, especially for those fraudulent activities where criminals need to access your credit. The premise of it is that you can freeze your social security number with all 3 credit bureaus. No one can process or apply for credit under your social security number without your permission. If you want to apply for a loan, you have to unfreeze your social security number and provide the date you want them to freeze it back. Usually, there is a fee to unfreeze, the best approach would be to unfreeze all of them since you do not know which report the company is going to use.

This option has surely provided me with the most security and peace of mind, especially knowing for any credit applications, the credit bureaus have to first secure and process my passwords before unfreezing my credit.

The above methods are not exhaustive but they have surely given me a sense of control and know-how and what to monitor.

.

9. Top Credit Score Questions

There are many issues, challenges when it comes to getting a great credit score. The below questions are some of the top questions and or concerns, but one of the surest way is to create a research, set a goal then create a plan.

.

Can I check my Credit Score For Free?

Yes you can check your credit card for free once year. Just make sure that the free credit report has all 3 credit bureaus listed.m, which are Equifax, TransUnion and Experian. You can pull your free credit from the link below:

https://www.

annualcreditreport.com/ .

What is Considered a Good Score?

Credit score has three digits and and determines if your are credit worthy to borrow money. The higher your score, the more trustworthy you are and more likely to get cheaper rates. Below are the different credit score categories:

Rating Score Poor 300 – 579 Fair 580 – 669 Good 670 – 739 Very Good 740 – 799 Exceptional 800 – 850 .

How Can I Quickly Raise My Credit Score?

The best way to raise your credit score is to pay off debt as quickly as possible. It is best to start with debt that you can completely payoff as it will be reposted as paid off on your credit report and this raises your score. Below are some tips to consider

- Make an extra payment each month

- Implement debt repayment method such as snowball

- Refinance your debt in order to save money on interest

- Carefully use balance transfer process

You can get all your 3 reports from the link below. Additionally, you can access your free report once a year, thereafter there is usually a fee associated. https://www.

annualcreditreport.com/ .

Can I Buy a House with 661 Credit Score?

A 661 credit score is considered to be fair rating and most lenders approve mortgages with that score.

Before applying for a loan, make sure to conduct your research and confirm with your desired lender which credit score they normally approve for, once that’s done you can implement tips to quickly increase your credit score.

Read this article on How to Increase Your Credit Score:

How Is Credit Score Calculated?

Credit score is also referred to as FICO score, which a 3 digit that ranges from 300 to 800. The higher the score, the more credit worthiness you are and more likely to get approved.

Below are the requirements needed to calculate your FICO Score

Payment History 35% : The best way to manage this section is to pay your bills on time and the worse case scenario is not to go past 30 days late. The longer it goes past the due dates, the worst it becomes, for instance 60 days past due is worse than 30 days past due.

Amount Owed = 30% : The best way to manage this option is not to owe over 30% of your total balance. For instance if you have a $1000 x 30% = $300. The best option to manage your credit under this section would be to not go above $300.

Length of Credit = 10% : The longer your credit history is, the better. The best way to manage this section, would be to payoff account but do not close them. Be mindful of the credit cards that are paid off and still open, if they are not used in certain time frame the credit card company may close it. Therefore, it is best to rotate your credit card usage.

New Credit = 15% : If you are in the process of trying to use your credit, opening many new accounts is a sure way to decrease your score. The best manage to process would be to have credit cards or loans that actually benefit you. For instance, get a credit card that has great benefits, such as cash back, mileage or any other service that is to your advantage.

Credit Mix = 10% : There are different types of loans and the more different they are, the best it is for your score. Some of the types loans include cards, retail accounts, installment loans, finance company accounts and mortgage loans.

You do not have to apply for all loans, but a mixture of them would serve you best

.

Why is Credit Score so Important?

The higher your credit score the better it is easier to get approved for any loans you may apply for. In addition to applying for loans, your credit score is now used by fellow employers to determine if you are an approved job candidate.

.

How Can I Wipe my Credit Clean?

The best way to clean your credit clean is to first pull all your 3 credit scores and dispute any errors. The second thing would be decrease and work towards on paying off any outstanding balance. The third step would be to learn how to manage your credit score and constantly adjust accordingly. Read question # 7 for am how to manage your credit.

.

Can You Cheat Your Credit Score?

You cannot cheat on your credit score, but you can apply tips and tools that may help you to quickly raise it.

Summary

Honestly, there are many different methods on how to improve and secure your credit score, but the most important aspect is getting yourself educated on the most basics statics and start applying them. Securing your credit can easily help to mitigate and protect you from external threats such as identity theft while understanding how your credit score works in improving your score and ultimately help you save money.

Cheering To Your Success

Brenda | www.DesignYourFinances.com

Let’s Connect on Social Media! | Pinterest |

–

QUOTE OF THE DAY

-

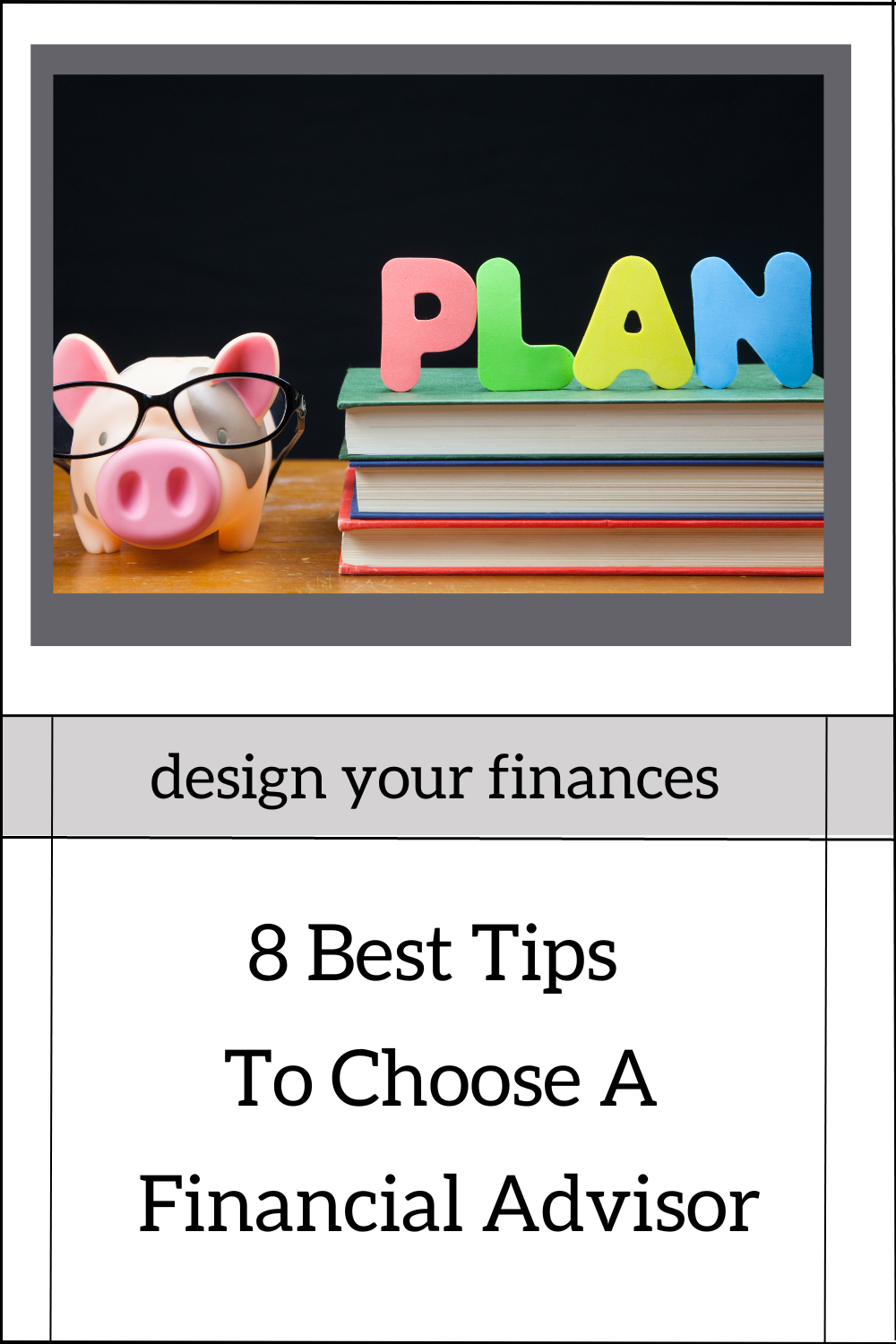

8 Best Tips To Choose A Financial Advisor

Financial advisor is a subject expert matter or specialist who manages money for individuals and should conduct fiduciary duty when providing advice.

Financial advisor is a subject expert matter or specialist who manages money for individuals and should conduct fiduciary duty when providing advice. Selecting a financial advisor is one of the most significant financial decisions you’ll ever make. The right advisor can provide invaluable guidance, helping you navigate the complexities of wealth management, investment, retirement planning, and more.

However, the wrong choice can have costly consequences. In this comprehensive guide, we’ll delve into the eight best tips to help you make a well-informed decision when choosing a financial advisor. From understanding your financial goals and objectives to conducting thorough due diligence and asking the right questions, these tips are designed to empower you to find an advisor who aligns with your unique financial needs.

Whether you’re seeking assistance with retirement planning, investment strategies, or comprehensive financial planning, these insights will guide you through the selection process, ensuring that you entrust your financial future to a qualified and trustworthy professional. So, let’s embark on this journey to discover the eight essential tips for choosing the right financial advisor, one who can help you build a more secure and prosperous financial future.

.

Broker vs Financial Advisor

Both roles are part of the financial sectors and are interrelated, but their objectives are different and they create a check and balance format. A broker is a middleman who arranges the sale between the buyer and the seller for a commission when the sale is done. Brokers are associated with a brokerage firm such:

- Etrade

- TD Ameritrade

- Charles Schwab

For a broker to be fully licensed and recognized by the state they have to complete various exams and obtain licenses.

Requirements include:

FINRA A broker must be sponsored by a FINRA registered firm or regulatory authority (FINRA – Financial Industry Regulatory Authority. Anyone directly or indirectly engaged in the banking or securities business is controlled by FINRA) LICENSES

a broker is required to pass the Series 7 and Series 63 exams Series 7 Exam covers – financial topics relating to the trading of many different types of securities

Series 63 – also covers the trading of securities, but focuses on state rules and laws.

.

Financial Advisor or Planner

As stated above financial advisors offer services and guidance regarding your finances. A financial planner offers different types of services that include:

- Insurance

- Estate Planning

- Tax Planning

- Investment Management (among others)

Licenses

There are many different types of certifications, below are the type of certifications that a Financial Advisor can obtain. This is not an exhaustive list nor does it mean that acquisition of certifications is above any fiduciary duty given to any client

- Certified Fund Specialist

- Certified Financial Advisor

- Chartered Financial Analyst

- Certified Financial Planner

- Personal Financial Specialist

NASAA Licenses: Series 65 & Series 66 This exam tests you on basic economic concepts, investment knowledge, and understanding clients’ needs

.

Background Check

Having certifications should not be the only source of due diligence, in fact, it should be in addition to other factors that help you in understanding what to expect from your advisor.

There are many ways to conduct due diligence, for example through government websites such as BrokerCheck by Finra verify you can use the site to investigate if the firm or the broker has any fraudulent or other financial charges against them.

Related articles:

- Tools For an Income Blog

- Effective Personal Budgets

- 10 Effective Personal Budget Tips

- 10 Investments that Create Wealth

- How to Organize Your Blogging Business

- How to Save for Money for Big Events in Life

- How I Got a Six-Figure Raise 80k to over 150k

.

Securities and Exchange Commission (SEC)

The SEC main objective is to protect investors by providing a platform where the public can access and have the ability to research a broker or firm’s credibility. One can access if there were ever any financial crimes or material disclosures that may affect one’s decision in using that firm. In addition to protecting investors, the SEC is an independent federal agency that promotes fairness in the securities markets, and they monitor laws and regulations that all companies and individuals dealing with securities should abide by. There are more sections that are covered in the SEC Report and below are the main sections

Firm

Look for the disclosures section, this will list offenses and the associated fines that the organization was charged. This will give you a clearer picture of how the firm conducts business and if there is anything alarming you should be aware of.

Broker

The report will show:

- Licenses – it lists current ones

- Experience – number of years

- Examinations – list of the exams passed

- Disclosures – if they were fined or disciplined

- Employment – number of companies they worked for

.

Payments or Fees

There are numerous and innovative ways of how financial advisors or brokers get to charge for their services. Some offer consulting fees, and then selection of a package or service would be the initial start of the relationship and this may come with ongoing charges. Below are some types of charges an advisor may use.

Commission Only

This will mean you will pay the commission upfront from your initial investment. If you invest $75,000 and the fee is s its 10% commission, then your broker fee will be $7,500.

Fee-Only

This is an hourly charge and usually, fees are based on the list of services they offer

The advisor is more of a consultant who has various services as well as charges. Sometimes you may find they are self-employed and not part of a big firm. For their services, they offer varying methods of charging such as hourly, flat fee or a retainer fee.

The best approach is to research and calculate the most effective methods for you. After all, you are paying a significant amount of money.

Fiduciary vs Broker

You would think the word advisor within a title would mean you get the best quality service that puts your needs and requirements above any fees. Unfortunately, that is not the case, you need to ask and verify if your advisor is a FIDUCIARY ADVISOR.

Fiduciary Advisor – means that the first priority is providing you with advice that is in your best interest and not advice that is driven by monetary gains (on your advisors part)

Risk Tolerance Level

When you start to invest whether passively or aggressively it is vital to understand your risk levels. This has been advocated many times that the earlier you invest the better and this component is relative to the risk levels you can take. For instance, if you are younger you can take more risk with your investing strategies and past a certain point, you become modest. High risk, high rewards can be true in investing but be cautious with your decisions. This is where you need a fiduciary financial advisor because your monetary objectives are at the top of their concerns.

It is imperative to know how your financial advisor is getting paid as this creates various objectives. Your goals and your advisor should be aligned, but we have seen numerous examples where people have lost their life savings and yet financial advisors keep getting richer.

.

Top Financial Advisor Questions

These are some of the questions or concerns that were most asked, additionally, this is not an exhaustive list. The best approach would be to formulate questions based on what you want to achieve, know your goals and your desired financial plan.

.

What do financial advisor do?

Financial advisors usually are accredited professionals in the financial sector who use their knowledge to advise clients regarding financial planning. During the financial planning, financial advisors fiduciary duty is to advice clients of the type of Investment that are in the client’s best interest and theirs them. Their primary goal should be creating a financial plan that will help you reach your financial goals such as retirement or buying a house.

Is it Worth to Get a Financial Advisor?

There are different types of financial advisors. The best ones would be fiduciary advisors as they advice based on your best interest and not just focus on selling products. Fiduciary advisors can be the best source of information of what are the best investments to include in your portfolio. Additionally, they can map out your financial strategy on to reach your financial goals.

KEY NOTE: With any financial advice, please conduct though research as any investment carries its own set of risks

Do Financial Advisors Charge a Fee?

Financial advisors the do charge fee. Usually most of them their fees are based on the amount of investment you have and these are fee based advisors. There are different formats of how they charge their clients such as percentage based for Assets Under Management (AUM) or fee based which is usually based on an hourly rate. Regardless of which type of a financial advisor you choose, it is advisable to search for a fiduciary advisor.

KEY NOTE : There is so much free information available, it is best to do your research first before consulting an advisor

Can You Trust a Financial Advisor?

There are many financial news reports about investors being swindled by financial advisors, that is the main reason to be well researched and educated when it comes to selecting an advisor. Financial advisors are accredited professionals and they are monitored by SEC (Securites Exchange Commission). For continuous monitoring by SEC they have to be registered as well as the company they work for.

It is a good practice to research your financial advisor before conducting any business with them. The SEC has work history of registered advisors, which list any financial penalties, disclosures and or if they are still accredited. This is the best place to safeguard your investment.

Can I Talk to a Financial Advisor for free?

Most financial advisors they have associated fees for their services from consultation to managing your assets. In the recent years, there has been an influx of available information as a result you can easily access information.

What to Do Before Meeting a Financial Advisor?

- Know the Type of Advisor You Selecting (fiduciary)

- Know the type of Charges You Will incur for the consultation & When Investing

- Know Your Financial Status & Prepare Your Personal Financial Statement, P&L, Balance Sheet (simply just tally all your assets & debts)

- Have a List of Your Financial Goals

- Do a Detailed Research of the Firm & the Financial Advisor

- Check Out Your Financial Advisor’s Credentials

- Clearly State Your Financial Goals Timelines and Deadlines eg retirement, college, buying a home

Questions to Ask Your Financial Advisor?

- How will communication be distributed

- How much are the charges for Assets Under Management (AUM)

- Ask Your Financial Advisor if they are a Fiduciary and what are their Duties

- Ask them how often the re-adjust, monitor and advise of better types of investments

- Ask them for different investments strategies to best meet your financial goals.

- Ask the rate of return his/her clients have achieved

- Ask how they solicit investments and what threshold they aim for

- Ask and understand the different risk and tolerance levels

- Ask the different types of investments and their tax requirements and how best to protect them

Summary

Due diligence should be done, but above all, you should know the warning signs of bad financial advisors. To best equip yourself, one should know the type of investment you are interested in and educate yourself.

Keep track of any current news that may be reported about your advisor, most get to know the bad news when it’s too late, yet you can keep abreast with any negative news that may have mandatory disclosure. Use competition to your advantage, research various financial advisors and learn ways how the financial market is safeguarded, such as new law, regulations and or adjustments to your portfolio.

There is certainly more ground to cover when it comes to researching which brokerage firm and or broker, that best suits you, but the best approach is to constantly keep a watchful eye on whoever is managing your money.

.

Cheering To Your Success

Brenda | www.DesignYourFinances.com

Let’s Connect on Social Media! | Pinterest |

.–

QUOTE OF THE DAY

-

11 Top Investments that Create Wealth

Wealth management or investment management is the process of financial planning which aims to protect, grow and distribute financial assets.

Wealth management or investment management is the process of financial planning which aims to protect, grow and distribute financial assets.Wealth management starts with taking charge of your personal finance. It has its own challenges and most of the time it’s catching up or busy paying off debt. We all work hard for the money, but we certainly want to make sure the money works at least twice as hard as we do.

There is so much information that supports the fact of early investing, saving and preparing financial goals, but in all honesty, it is overwhelming to decipher all the different forms of investment securities. Below is a list of various methods of investing and the vehicles used to invest, though it’s not exhaustive hopefully it provides some helpful information.

Investing is the cornerstone of wealth creation, and the right investment choices can pave the path to financial success and security. In this blog post, we will explore 11 top investments that have the potential to generate wealth. Whether your goal is to save for retirement, build a nest egg, or achieve financial independence, these insights are designed to equip you with the knowledge to make informed investment decisions. By understanding the potential risks and rewards of each investment option, you can create a diversified portfolio that aligns with your financial goals and aspirations, setting the stage for a more prosperous and secure financial future.

Please, with any financial information do your research and consult a financial advisor.

.

Options

Simply, options are buying and selling of contract securities with an aim to make a profit. An option is a contract that gives the buyer the right to buy or sell a security, such as stock or exchange-traded fund (EFT) within a specific period of time. The price of an option is called a premium, options are commonly used in the stock market, futures, forex, and other markets. Most investors use contract options to hedge positions for both buying and selling the stock.

Call Option – is the buyer who has the right to buy the stock at a certain price

Put Option – buyer has the right to sell the stock at a specific price before it the options expire.

Strike Price – this is when buyers can exercise their right to buy or sell at the strike price

.

Annuities

This type of investment is between you and the insurance company, where the company makes periodic contributions to you sometime in the future. You can purchase the annuity in a single transaction or make a series of payments known as premiums. There are varying forms of annuities which include fixed, variable and indexed.

Fixed Annuities

You have a guaranteed rate of return, and the payout of your payout rate is based on your age, life expectancy, and prevailing interest rate. Even though the annuity states fixed, the annuity can change over time, it is best to understand your contract. The payout can be for an entire lifetime or you can choose another time period. Something important to note is your taxes, assets in a deferred fixed annuity, your investment grows tax-deferred.

Variable Annuities

This form of investment allows you to select from various investment choices, such as mutual funds. The variable annuity rate of return changes with the stock, bond and money market funds, in addition, the variable funds are also compared to mutual funds because of the similar investment features. The structure of a variable annuity offers three basic features, which include:

- a death benefit

- annuity payout payout

- tax-deferred treatment of earnings

Variable annuities do not provide any guarantee that you will earn a return on your investment.

The best approach is to fully understand all the terms, fees, expenses and additionally the prospectus.

Indexed Annuities

This type of investment includes both fixed and variable annuities. They offer a minimum guaranteed interest rate, additionally, this type of investment is more complex in regards to the other two. They are also known as “equity-indexed annuities” or “fixed indexed annuities” mainly because they have characteristics of variable and fixed annuities. Index annuities are not simple to understand and one of the complexities is that there are several methods to calculate gains, this may be difficult for investors to compare one indexed annuity to another.

Best approach before purchasing an index, it is best to fully understand each feature and how it works, as this may have a greater impact on our retains.

.

Bonds

A bond is simply a loan that an investor makes to the corporation, government or any other organization and in exchange, they get paid an interest rate over the specified amount of time.

The structure of a bond is similar to a lender and a borrower. There are many different types of bonds and the quality of “borrowers” varies as well, such as corporate bonds, municipal bonds, treasury bonds or agency bonds. Bonds also carry various risk factors some of them include interest rate risk, call risk, default and credit risk. All these risk factors are associated with the possibility of you losing your money.

Just a simple rule of thumb, when interest rates fall, bond prices rise, and when interest rates rise, bond prices fall. Make sure you evaluate the quality of your bond, as all bonds are not valued the same, therefore different credit ratings.

Related articles:

- Effective Personal Budgets

- 10 Effective Personal Budget Tips

- 10 Investments that Create Wealth

- How to Save for Money for Big Events in Life

.

Mutual Funds

This type of investing offers diversification to an investment portfolio and offer various advantages instead of purchasing individual stocks or bonds. A mutual fund is a professionally managed investment fund that pools money from many investors to purchase securities.

The money is used to purchase various securities instruments such as stocks, bonds or short-long term investments. You can find more details of a mutual in a document called a prospectus which includes investment strategies, risk profile, management or fees. Here is how mutual funds works, any profits achieved are shared after expenses, and the payments to its shareholders are known as income distributions.

Capital gains are achieved after selling an investment in its portfolio at a profit and are passed to shareholders (you) as capital gains (after expenses are deducted) You would have to pay taxes on the fund’s income distributions, unless if you have a tax-deferred or tax-free account. Best to communicate with your tax advisor or financial advisor of what is the best option for you to take.

Exchange-Traded Funds (ETF)

Exchange-traded Funds (ETF) are a combination of mutual funds and conventional stocks. This may be a bit confusing since the investment vehicles are similar. Below are the distinguishing factors of ETF’s being pooled investments, they offer the investor an interest in a professionally managed and diversified portfolio investments. ETF’s shares can be bought throughout a trading day at varying prices.

There are many different types of ETFs and they are not created the same.

Most ETFs are registered with the SEC as investment companies, but keep in mind that ETF’s that invest in commodities, currencies (and other investments) are not registered investment companies. The management style can either be active or passively tracked. Passively managed ETF’s aim to achieve the same return as the index that they are tracking.

.

Stocks

This is the most known form of investment when you buy into a company, that is buying stocks or shares of that company. There different types of stocks but the main ones are preferred stock and common stock. Preferred stock is when you get dividends and the common stock does not issue dividends.

When you evaluate the stock, the EPS (earnings per share) is one indicator of the company’s current strength. To either buy or sell the stock one would need a brokerage account and the stockbroker at the firm will have to execute the trade for you.

.

Roth IRA

There are many types of investment account and a Roth IRA offers multiple benefits and has set rules one should follow. Contributions in a Roth IRA and investment earnings grow tax-free, meaning there’s no tax on your Roth IRA withdrawals in retirement. Unlike in a Traditional IRA, withdrawals in retirement are taxed as income. Roth IRA can be opened at a brokerage or bank and you can make a selection of what type of investments to make, such as mutual funds, stock, bonds etc.

Benefits of a Roth IRA

- You can withdraw the money you contributed without tax or penalty at any time, with no restrictions, because you’ve already paid taxes on that money. (be mindful of this rule because you can be penalized if you withdraw earnings on your investments, but not contributions)

- There is no age limit to opening a Roth IRA, but there is a limitation in what you can contribute each year

- This is one of the most advantageous reasons for opening a Roth IRA, your money grows tax-free and the withdrawals are tax-free as well.

401(k)

401(k) is an employee-sponsored retirement option. Usually, an employer matches your contribution up to a certain amount, for instance, every dollar you put into your 401(k) an employer can match every dollar up to a certain amount.

401(k) Facts below

- You have less control of investment strategies and or options

- Just like Roth IRA, there are yearly imposed contribution limitations.

- Distributions in retirements are taxed as ordinary income unlike Roth IRA

- It has a high annual contribution limit (there is a maximum contribution limit the government sets each year)

Most financial advice supports the fact that when it comes to 401(k) do not leave free money on the table, contribute up the amount your employer is matching and the rest fund your Roth IRA as your money will grow tax-free.

.

Top Wealth Building Questions

These are some of the questions or concerns that were most asked, additionally, this is not an exhaustive list. The best approach would be to formulate questions based on what you want to achieve, know your goals and your desired financial plan.

.

What Should I Invest in to Build Wealth?

The best investment that create wealth includes investment have that a high rate of return and low risk. The more traditional retirement investments such as 401(k) or IRA, they normally take a what feels like lifetime to accumulate and grow.

The best approach is to determine which investments work with your time frame and which ones can be more aggressive in growth.

Below are some aggressive investment

- Starting a business

- Options

- Real Estate

- Index Funds

Can Investments Make You Rich?

Yes. Comparing to the standard interest rate you get from a savings account, you can easily earn more money with a diversified investment portfolio. Just like with any investment, it is advisable to research the type of investment that will yield the highest rate of return as well as the risk associated.

Another factor to consider is how aggressive you want your investment portfolio to be structured. Usually, the more aggressive, the higher the returns and the higher the risk.

KEY NOTE = Index Funds are considered to be on the conservative side but they tend to outperform 401(k)

What does it mean to Build Wealth?

Wealth building is the process of creating multiple investment strategies that in turn consistently generate multiple long term income. Financial planning is the first step to creating a plan that can actually yield results. It takes into consideration your target date and determines how much periodically invest in order to meet your target.

How Can I Build Wealth Fast?

In order to build wealth fast it requires a solid financial foundation to start with. The best approach is to implement the basic financial fundamentals such as budgeting, paying off debt and setting financial goals. Once you have set your financial goals, actionable tasks would be a priority such as aggressively increasing your income. The more disposable income you have, the more you can allocate to multiple investment streams

How do the Wealthy Stay Wealth?

There are various financial strategies that the wealthy implement to make, grow and safeguard their assets. The below list only highlights the few strategies.

INCOME – The wealthy generally have multiple ways to generate income and not only that, they implement strategies that compound their earnings.

- FOR INSTANCE: Your 401(k) earns about 4% per year while SPY earns about 10%. The above example shows why the wealthy can easily compound their income mainly due to strategies that accelerate their growth

TAXES – Many wealthy people they create financial instruments that legally allows them to pay lower taxes. Such as different company entities LLC / S Corp / Trust etc. This is one of the greatest tool they have as their tax bill is lowered that means they have more disposal income.

ASSET PROTECTION – There are many ways to set up a business. The correct formation of your business can also protect your investments. For instance, if you have a business and it gets sued, as a sole proprietor you can be personally sued as well unlike an Limited Liability Company (LLC), only your business sued and not your personal asset.

INHERITANCE – This is one of the most debated topics regarding generational wealth, on how to pass your wealth to the next generation with limited tax exposure. Through financial planning, they are able to different types of company structure that allow them the easily transfer wealth.

What Should I Invest In to Build Wealth?

Wealth building is all depended on your goal and time frame of what suits your needs. Usually the more time you have towards your target date, the more aggressive the investment strategies are applied. For instance, if you are closer to your target date then the investment strategies selected are more conservative instead of being aggressive.

The best approach to verify in which type of investment create wealth, first identify which investments are available to you (as some require accredited investors), thereafter, verify how much money is needed to start as well as educating yourself.

How do You Build Wealth from Nothing?

The first step to building your wealth is to first take note of your current financial status and then decide what your financial goals are. For instance, this may be paying off debt, creating passive income and retirement. All these are financial goals.

The second step would be to know your exact debt and paying it off, while simultaneously creating passive income that increase your disposable income.

The third step would be to investigate which investment strategies fit your model. The power of compound interest is one of the most desired tool to gain wealth.

The fourth step would be to constantly monitor by adding or removing investment strategies that are not yielding your desired performance.

What is the Key Ingredients in Building Wealth?

The main ingredients of building wealth includes: Discipline. Knowledge and Disposal Income.

Discipline: this is an essential tool when it comes to building and maintaining wealth. Tools like budgeting and financial planning are advantageous to this section

Knowledge: before starting to invest in any strategies, it is best to fully understand the risks and rate of return. The idea is your money to generate more money and not burn it. PLEASE DO A THROUGH RESEARCH BEFORE INVESTING

Disposal Income: as your income increases or investments yield dividends it advisable to reinvest it instead of funding new lifestyle demands.

What is the Best Way to Accumulate Wealth?

The best way to accumulate wealth is to first access your financial status and then determine your financial goals. Debt is the most aggressive form of wealth depletion, therefore, it is better to pay it off as soon as possible.

The best investments that creates wealth are investments that bring a high rate of return and have the ability to hedge and manage risks effectively.

There are different types of investment but they mainly fall under two categories, ones that generate income passively and ones that you actively manage.

Regardless of the option you choose, there are 4 main principles of becoming wealthy. Make. Save. Invest. Debt Free

Where Should a Beginner Invest?

The best approach is to start with investments that are generate income passively and don’t require massive capital. After paying your debt or at least having a strategy to paying off, it best to start by educating your self in the different types of investments and associated risks. Below is not an exhaustive list but can be a starting point:

- Retirement accounts

- Index Funds

- Mutual Funds

- ETF

How do You Build with Little Money?

The best way to build wealth with little money is to look for investments that do not require massive capital to start with and getting a decent rate of return.

Some investment to consider include

- index Funds

- High Yield Savings Account

- Stock Trading

- Side Hustle

Summary

There are many types and ways to invest your money in, the most imperative aspect is to research, determine your level of risk tolerance and start investing. The best approach is to understand the rules, especially, contribution limits, withdrawals and or penalties.

.

Cheering To Your Success

Brenda | www.DesignYourFinances.com

Let’s Connect on Social Media! | Pinterest |

.–

QUOTE OF THE DAY

-

10 Personal Budgets That Save Money Fast

Personal budgets includes the process of managing finances by allocating, forecasting expenses and saving money.

Personal budgets includes the process of managing finances by allocating, forecasting expenses and saving money. Managing personal finances is a task that is both essential and, at times, challenging. Crafting an effective personal budget is the cornerstone of financial stability and a key to achieving your financial goals.

Designing your finances requires one to be financially savvy and that requires various aspects such as research, budgeting, investing and truthfully, discipline. The form and process of budgeting have many components and thus making it challenging to maintain a successful working budget.

Below are some different types of budgeting methods, tips, and strategies that can be easily implemented. However, a budget is not just about tracking expenses; it’s a powerful tool for saving money quickly. In this comprehensive guide, we will explore the strategies and tactics that can help you create a personal budget that not only keeps your spending in check but also accelerates your savings. From setting clear financial objectives and tracking your expenses to prioritizing savings and making frugal choices, these tips will equip you with the knowledge and skills to build a budget that can swiftly bolster your financial health. Whether you’re looking to build an emergency fund, pay off debt, or work towards a specific financial goal, a well-structured personal budget is the key to achieving those objectives with speed and efficiency. So, let’s dive into the world of personal budgets that save money fast and pave the way for a more financially secure future.

.

1. Actions Items

In order to successfully implement a budget, there are action items that one must conduct before choosing a budget that works for you.

Setting Budget Goals

You have to identify why you need to have a budget and state your objectives. Is the budget targeted for a long-term goal or short term, what purpose is it going to serve, are you paying the debt off, saving for a house and or boosting your saving or investments?

Know Your True Income

This is one of the questions many people have a hard time answering. How much is your gross and net income? This should be a starting point, as it clearly provides you with the disposable income you have. Additionally, this gives you a clearer picture of what your deductions are, knowing this information, will help immensely as you are able to adjust how much you are being taxed, which can ultimately increase your take home. The objective is to not overpay in taxes, therefore, it is best to consult a tax accountant and find ways that can decrease your taxes. NB: Tax evasion and implementing methodologies that reduce your taxes are NOT the same thing. Do not break the law, that is why a tax accountant will be instrumental in assisting you in finding LEGAL SOLUTIONS.

How Much Your Debt Is

This activity can be very stressful, especially when you have to itemize all your debt which can create a sense of being overwhelmed. Whether you itemize your debt by the lowest to highest interest rate, amount and or the number of payments, it is imperative to list all your debt and have an accurate amount of what you owe. This provides such a great blueprint, especially when you start paying off your debt, your action plan is halfway in motion.

Set Timeframes

For any goal to be successful, there have to be set realistic timeframes. Setting extremely demanding goals in a short amount of time is clearly the best way to sabotage your efforts, leading to being overwhelmed and failure. Know the exact amount of money you can allocate towards your debt each month. For a goal to be successful, it is best to follow a methodology that you can easily implement, such as S.M.A.R.T Goals

Specific identify your goal, for instance, payoff credit cards, then the student loans Measurable be able to track your progress and set your milestones. Attainable do not overstate your ability, as this may lead to disappointments. Set goals that you can achieve, such as payoff 1 credit card at a time. Realistic sometimes achieve your goal, you may need to think outside the box, such as getting another job or starting a side hustle, all these contribute to creating realistic goals Timely set dates, deadlines or milestones that allow you to succeed. .

2. Time Budgets and Personal Budgets

This type of budget is based on a specific timeframe such as a week, month or year and the goals vary from each time period to the other. Below are some examples,

Weekly Budget

This can be associated with weekly allowances which may include transactions that more frequent than the others such as, gas, groceries or getting your nails done. Having a weekly budget allows you to have some spending money and most importantly use only what is allocated.

Monthly Budget

Creating this budget focuses on transactions that are paid monthly. The budget normally includes expenses such as car note, mortgage, utilities. These expenses tend to be fixed and are on a set due date. This makes it much easier to create a budget because they hardly have any new surprises in the way they are formatted.

Yearly Budgets

Yearly budgets are expenses that are paid once a year and or quarterly and need advance budget planning and enough money allocated to achieve the goal. For instance, property taxes can fit into this category. Though some states pay property taxes more than once a year, it is surely a bill that you have to plan for. This bill is based on the value of your home, therefore, in some cases, it can increase over time. When you fail to adequately budget for this expense among others, this can surely, have a true financial burden which can lead to a tax lien.

Long Term (over a year)

Long term budgets are expenses that need more than a year of planning, funds allocation and or investing. Some of these expenses may be grouped either short or long term. When you define your expenses, it is best to accurately state your abilities. For instance, short term (though it may be longer than a year) can include expenses, such as saving for a down payment for a house or a wedding. Usually, some experts define short term objectives as five years or less.

Long term budgets are expenses that need funds allocation of least 5 years and more. These expenses include retirement and or saving for college. These expenses are well funded and increase in value if contributed consistently and for a long time. Every dollar counts, especially when setting up goals.

Due to the different types of time budgets, it is imperative that your planning and allocation process truly caters to all needs. The above-listed expenses in each category, are true expenses in any household and have to be carefully planned for. Regardless of your income level, we all have expenses that require true allocation management.

.

3. Cash Only

What is a Cash Budget, how does it help with budgeting, how do you plan it? These are the questions that need to be answered before applying this method.

What is a Cash Budget – this is a process where you only use cash for all your daily needs and if you run out of money, you DO NOT reallocate additional funds. A debit card can be used for this method, but this can really set you off if your debit card is attached to your savings or another account that has money in it.

How does it help with budgeting – the idea in any budgeting process is to stop excess spending and or incorrectly using your money. You already work so hard for your money, have multiple deductions, it only helps if your money works harder than you do. The most imperative aspect of this type of budgeting is to discipline spending habits by creating intended spending.

How Do You Plan for it – the best approach is to start small and then gradually increase your budgeting process. The first step is to identify expenses and or categories that you can easily pay with cash, such as groceries, lunch, transportation. Thereafter, you need to set a time-based approach such as, when you can withdraw your cash and how long the money should last. Tracking your progress is vitally important, therefore, constantly tallying your expenses is a big help.

TIP- use your debit cards, only if you are able to keep to your goal, as it may become hard to manage.

Related articles:

- Tools For an Income Blog

- Effective Personal Budgets

- 10 Effective Personal Budget Tips

- 10 Investments that Create Wealth

- How to Organize Your Blogging Business

- How to Save for Money for Big Events in Life

- How I Got a Six-Figure Raise 80k to over 150k

.

4. The Envelope System

This method has the same setup as the cash budget but it is more detailed and can include a wide range of categories. All or most of your bills are paid through the envelope system.

How Do You Plan for it – the first step is to organize your expenses into categories, then allocating the funds to that category. For instance, your categories can include but not limited to, groceries, utilities, transportation and or clothing. Next step, is to aggregate the amount of each category that is going to last you till the next cash distribution in that category, for instance, you allocate funds into your envelopes every 15th of each month – that means no topping funds until the next due date, the 15th of next month.

How to Succeed – by tracking your expenses and carefully allocating the correct amount. Usually, budget shortages occur when there is a mismanagement. You may need to reallocate more funds in one category than the norm because it might be a necessity. For instance, utilities usually go up in summer months and that is reflected in your bills. You may try to eliminate some expenses and or reducing other categories such as clothing.

.

5. Bare Budget

This type of budget is only for bare necessities. It does not include any additional expenses such as luxuries, fun or social. As the theme continues, the first step is to always list your exact expenses.

When to Use it – bare budgeting is an extreme form of “money discipline” it does not allow any room other than what is required to survive. Usually, this form of budgeting is used when there is an aggressive goal and or limited timeframe, such as paying the debt off or saving for a down payment. Since it is extreme, it can be hard to maintain it in the long term.

Two forms of Bare Budget – personal finance is all about understanding and tracking where your money is being allocated. This is more enhanced with the Bare Budget, mainly because there are two forms, emergency budgeting or cutting back budgeting. Emergency budgeting is trimming your budget to only survival necessities such as food, shelter. Cutting Back Budgeting is when you still cut down expenses but also have room to allow some of “luxuries” such as entertainment, maybe one vacation per year. Of course, with cutting back budgeting, it should be planned in advance.

.

6. The Debt Free Budget

The above-listed requirements for the other budgets are the same for this one, listing your expenses first. The Debt-Free Budget supports the theory of saving first and not getting to debt.

How it Works – the success of this type of budget is to save first the required amount and then purchase what you need. If you cannot buy it with cash, you cannot afford it. This type of budgeting works well with gifts, vacations. At the beginning of the year, you can fund your budget in small increments, this really helps as the contributions are much smaller compared to last-minute payments.

How to Succeed – the main purpose of this budget is NOT TO GET INTO DEBT. Usually, the justification of expenses is a major driving force of getting into debt. For instance, if buying gifts or vacation, calculate the total cost, then divide into manageable installments.

.

7. Percentage Based Budget

This budget is framed and calculated from a percentage-based basis. You allocate a certain percentage for each main category, the idea behind it is that you cannot go above your set percentage. For instance:

Fifty percent – of your take-home goes toward needs and necessities such as shelter, food, utilities, debt repayment. It is better to have most of the allocation towards debt repayment and the reminder on other categories.

Thirty percent – of your take-home is spent on wants, such as clothing, eating out, hobbies. The idea behind this type of budget is to also enjoy life and not be so strict with money. Unfortunately, most have fallen short when it comes to this portion because needs and wants are ever-growing and usually accompanied by a rationale to go above the allocated percentage.

Twenty-Five Percent – this amount of money is allocated to start an emergency fund, savings, and retirement goals. This section is mainly based on creating a solid financial foundation.

.

Cheering To Your Success

Brenda | www.DesignYourFinances.com

Let’s Connect on Social Media! | Pinterest | .

.

QUOTE OF THE DAY

-

10 Crucial Budgeting Tips That Save Money

There are many personal budgeting tips regarding your money and personal finance, unfortunately, with the current inflation and economics it is getting harder to save and the debt is getting higher.

There are many personal budgeting tips regarding your money and personal finance, unfortunately, with the current inflation and economics it is getting harder to save and the debt is getting higher.Managing your finances and paying off your debt can seem like a never-ending process. The best method to eradicate debt or save for big expenses is to budget effectively. With the help of so many apps and tools, personal finance or budget management has become much simpler and there is no need for advanced accounting. Budgeting is more than just a financial exercise; it’s a powerful tool that can transform your financial health and help you achieve your financial goals.

The process of crafting and sticking to a budget not only provides a clear picture of your financial situation but also empowers you to make strategic decisions that can save you money. In this comprehensive guide, we’ll delve into crucial budgeting tips that have the potential to put more money back in your pocket. These tips encompass a range of strategies, from tracking your expenses and setting financial goals to controlling discretionary spending and prioritizing savings. Whether you’re seeking to reduce debt, build an emergency fund, or simply improve your financial well-being, these insights will equip you with the knowledge and tools to make budgeting a transformative force in your financial life. So, let’s embark on this journey to discover the budgeting tips that can help you save money, take control of your finances, and work toward a more secure and prosperous financial future.

.

Know Your Income

There are a lot of people who do not know exactly what they earn. If you are an employee, your paycheck is divided into different categories, mostly gross income, and net income.

- Gross Income: this amount is before any taxes & deductions

- Taxes: any state, federal or any other form of taxes

- Deductions: any amount that does not include taxes, medicare/ social security/ 401(k)/ health benefits

- Net Income: this is what you take home.

.

Itemize Your Expenses

Monthly budget(ting) tips, can only be effective if you know what you are spending your money on. The best methodology is to go by your bank statement, from the past three months. This helps you to have an overview of where your money is going. Below are different types of expenses: